Hello my friend,

Walk into any shop in Eastleigh, a hardware yard in Industrial Area or a small café in Westlands right now, and you’ll hear the same story: “Customers are buying less.” “People are delaying big purchases.” “Everyone is trading down to the cheapest option.”

This isn’t just anecdotal frustration. Hard data backs it up.

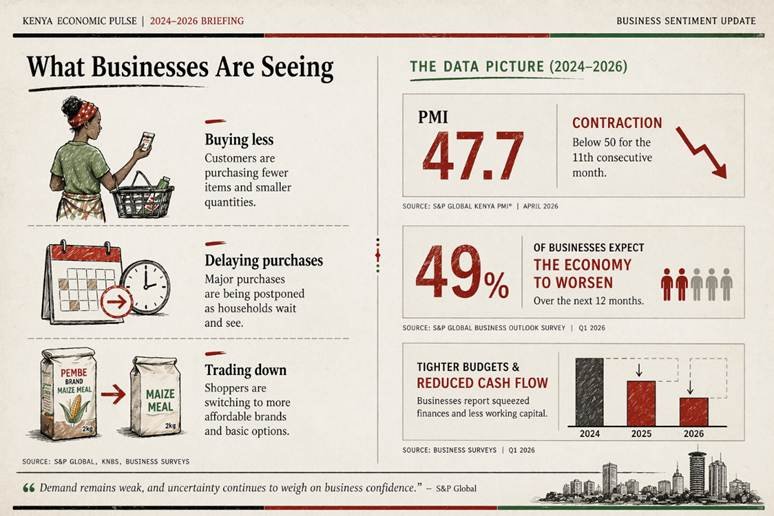

In March 2026, Kenya’s private sector slipped into contraction for the first time in eight months. The Stanbic Bank Kenya PMI fell to 47.7 (below the 50 neutral mark), with businesses citing weaker customer demand, tighter household budgets and reduced cash circulation as the main culprits. Output and new orders declined sharply as cautious spending took hold.

From sentiment across Reddit, Facebook groups and X: Kenyan founders and SME owners are saying the same thing – customers are holding back, stretching every shilling and prioritizing essentials over anything extra.

A recent poll showed 49% of Kenyans expect the economy to worsen in 2026, with fear of weaker personal finances directly translating into lower spending.

The core insight? Kenyan SMEs are not dying from lack of ideas or bad products. They are being squeezed by low consumer liquidity – people simply have less money in their pockets to spend freely.

What the Data Is Really Telling Us

- Constrained customer spending – Households are cutting back on non-essentials. Food and transport costs still dominate budgets, leaving little room for discretionary buys.

- Reduced cash circulation – People are holding onto cash longer, delaying big-ticket items (furniture, electronics, home upgrades) and choosing cheaper alternatives.

- Tighter household budgets – Even with inflation relatively stable around 4.4% in March 2026, the cumulative effect of high living costs, taxes and cautious borrowing means many families are operating in survival mode.

- Geopolitical ripple effects – The Middle East conflict has pushed up fuel and shipping costs, adding pressure without businesses being able to fully pass it on (because demand is too weak to absorb price hikes).

Retail, services and small manufacturing are feeling it hardest. Businesses report holding back on passing cost increases to customers to avoid losing already cautious buyers.

On the flip side, the informal sector and very small traders are adapting by offering rock-bottom prices, further pressuring formal SMEs who face higher compliance costs (eTIMS, validation rules, etc.).

The result? Many good businesses with solid ideas are struggling not because of poor execution, but because the money simply isn’t flowing in the economy the way it used to.

Why This Hits SMEs Especially Hard

SMEs make up the backbone of Kenya’s economy, but they have thinner buffers than big corporates. When consumer demand dries up:

- Inventory sits longer → cash tied up

- Margins get squeezed (you can’t easily raise prices)

- Credit becomes harder or more expensive to access

- Tax compliance feels heavier because every shilling counts

Many owners we speak to at Seal Associates say the same thing: “We have customers… but they’re spending far less than before.” The tax reforms and digital enforcement (eTIMS validation, automated checks) add another layer of pressure when cash is already tight.

Practical Ways to Navigate Weak Demand in 2026

You can’t control the broader economy, but you can control how your business responds. Here are battle-tested moves that are working for resilient Nairobi SMEs right now:

- Focus on Value and Affordability – Offer smaller pack sizes, bundles, or “essentials-first” options. Help customers stretch their budget while still choosing you.

- Improve Cash-Flow Discipline – Tighten credit terms, chase receivables faster, and build a small cash buffer. Even KSh 50,000 – 100,000 extra liquidity can make a huge difference when sales slow.

- Diversify Revenue Streams – Look for B2B opportunities, corporate clients, or export niches that are less affected by household spending. Some are shifting toward essential services or repair/maintenance work.

- Cut Waste, Not Quality – Review expenses ruthlessly but protect what keeps customers coming back. Early finance involvement (as we’ve discussed before) helps spot problems before they become crises.

- Stay Compliant Without Panic – Use KRA’s simplifications (daily TOT via M-Pesa where possible, Automated Payment Plans for arrears). Get your eTIMS and records tight – it prevents extra tax hits from disallowed expenses that you can’t afford right now.

At Seal Associates, we’re helping clients build simple cash-flow forecasts and compliance systems that fit tight budgets – so weak demand doesn’t turn into a cash-flow death spiral.

The Bottom Line: This Is a Liquidity Squeeze, Not a Lack of Potential

Kenya still has huge long-term potential – young population, growing digital adoption, and sectors like agriculture and services showing resilience. But right now, in Q1 2026, the dominant theme is weak consumer demand driven by low liquidity.

The businesses that will come out stronger are those that:

- Adapt quickly to cautious customers

- Protect every shilling of cash flow

- Stay compliant without letting it drain them

What are you seeing on the ground in your business or community? Are customers buying less, delaying or trading down? Drop your observations in the comments – let’s share practical ideas and support each other through this phase.

We’re in this together. Stronger demand will return, but smart moves today will determine who’s still standing when it does.

Prepared by Seal Associates Business Advisory Team